The Bank of England has hiked interest rates to 0.75%, their highest level in almost a decade on Thursday – sounds important but what the hell does it mean?

If you’re still of a relatively youthful age there’s a good chance interests rates have been at the same incredibly low levels for most of your adult life, so you’d be forgiven for not taking much notice.

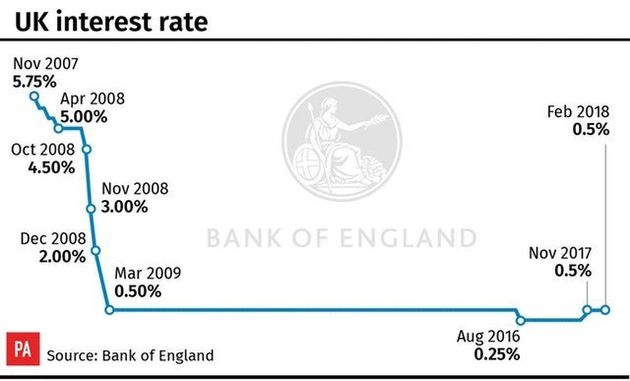

The move sees rates rise above the emergency low of 0.5% for the first time since March 2009 and marks only the second hike since the financial crisis, after last November’s quarter-point increase.

But with them likely creeping up a little this week, perhaps this is as good a time as any to get yourself acquainted with a fundamental part of monetary policy.

OK, let’s start with the basics:

What’s An Interest Rate?

Simply put, an interest rate is the amount it costs to borrow money.

This is always expressed as a percentage of the total loaned so the more you borrow, the more you pay.

They are typically calculated annually and so are called Annual Percentage Rates (APR).

What Does It Apply To?

The two biggest things in the context of the Bank of England news are mortgages and savings, two things millennials are notoriously short of.

Interest rates also apply when you buy something expensive like a car and pay in instalments, but for the purposes of this piece we’re going to ignore this.

How Does It Affect Them?

Mortgages and savings are basically opposites in terms of interest rates – what’s good for one is always bad for the other and vice versa.

If you have a mortgage then a lower interest rate is best, as it means the cost of borrowing the money you paid for your home with is lower.

If you have savings, a high interest rate is best as banks essentially pay you more each year – but savers shouldn’t expect to be able to boost their nest eggs in line with the national rate.

Many mortgages and savings accounts are set up on a ‘fixed-rate’ basis, meaning interest payments remain the same for a set period, regardless of any fluctuation.

Hang On, The Bank Pays Me?

Yup, lending money works both ways – when you deposit your paycheque in the bank, that bank is borrowing the money from you. They then invest this as they see fit, pay you a small fee – the interest rate – and promise to pay you back when you go to a cash point.

Why Is It So Low Right Now?

Back in November 2007 interest rates were 5.75% – great news for savers, less so for homebuyers.

Then the financial crisis happened and they were slashed from 1% to the emergency low of 0.5% in an effort to contain the fall-out.

How Does That Work?

The thinking is that if it costs less to borrow money, then more people will be willing to lend it – which in theory should stimulate the economy.

In 2009 the Bank of England combined lowering interest rates with quantitative easing – basically creating new money – in an effort to encourage lenders to get people buying things again.

Why Does It Have To Go Up?

Money is just like any other goods or service, in that the price you pay for it boils down to supply and demand.

Interests rates have been exceptionally low for almost a decade, but as the UK economy has strengthened, the demand for borrowing has increased.

As this happens, it’s only reasonable that lenders should be able to charge more and this is why the Bank of England plans to gradually increase interest rates.

But it also has the delicate job of balancing them, so that the cost of borrowing doesn’t rise too quickly.

If this happens then people may stop borrowing, potentially cancelling out some or all of the economic recovery since the financial crash.

What Does The Future Hold?

Can’t really help you there I’m afraid, too many variables.

Interest rates will go up as they can’t continue on what is essentially an emergency rate forever, but by how much and when is still up for debate.

But on Thursday the BofE was sligthly optimistic, keeping its forecast for UK growth unchanged at 1.4% in 2018, but upping the outlook to 1.8% in 2019.

What Do The Professionals Say?

Daniel Hegarty, CEO of leading digital mortgage broker Habito, said:

“Today’s hike was widely expected by banks and lenders who’ve already priced it in, so the cost of new mortgages are unlikely to shoot up immediately.

“The hike will be unwelcome news for the nearly 40% of UK homeowners on a variable rate mortgage, who’ll see their monthly payments go up. Increasing living costs and rising inflation has seen many households feeling the pinch, so even though a rise of 0.25 per cent seems small, it will have an impact on household finances.

“The best way to protect against rising rates is to see if you could be getting a better deal on a fixed rate mortgage. This will keep your repayments the same for 2, 3, 5 or more years, so that any future rate changes won’t catch you off-guard.

Gillian Guy, Chief Executive of Citizens Advice, said: “Last year 340,000 people came to Citizens Advice for help with their debts. Today’s move could be enough to push more households into the red.

“Household budgets are increasingly stretched. Our figures show 25% of UK households with a volatile income resorted to credit to pay for essentials such as food and bills.

“But the £209.4 billion borrowed from commercial lenders only tells half the story, with the extent to which people are behind on their household bills falling under the radar. The government must accurately record this so they can understand the true extent of people’s financial difficulties.”