We’re here to guide you through the coronavirus pandemic. Sign up to the Life newsletter for daily tips, advice, how-tos and escapism.

Stamp duty is the tax every homeowner dreads paying – especially when you’ve scrimped and saved to stump up a deposit, then swiftly realise you need thousands more for a lump sum tax payment.

With the economy in dire straits (the Resolution Foundation think tank warns the UK economy could shrink by 9.3% this year – the biggest annual hit in a century), chancellor of the exchequer Rishi Sunak has today made a statement with his recovery plan.

As part of this, he has announced a stamp duty “holiday”, which will take effect immediately and last until next March. So what does this actually mean for you – and is it a good deal?

What is stamp duty?

Stamp duty (or stamp duty land tax, SDLT) is a tax you pay if you buy a property or slice of land over a certain price in England and Northern Ireland.

The tax applies to both freehold and leasehold properties, whether you’re buying outright or with a mortgage.

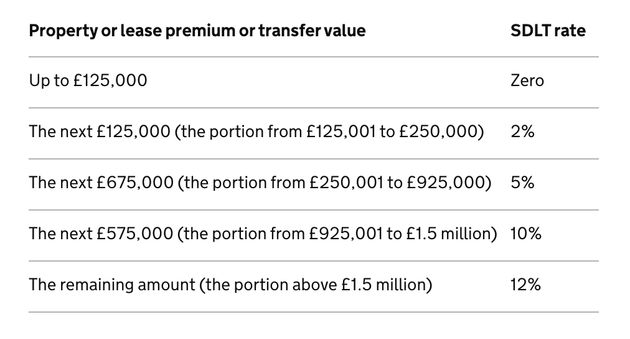

Before today, people had to pay stamp duty on homes over £125,000 or non-residential land and properties over £150,000. How much tax they would pay would go up as the value of the property increased.

So, if you were to buy a house for £275,000, the stamp duty tax you would need to pay would be as follows:

- 0% on the first £125,000 = £0

- 2% on the next £125,000 = £2,500

- 5% on the final £25,000 = £1,250

- Total stamp duty tax = £3,750

Is it the same for first-time buyers?

There were separate rules in place for first-time buyers, who wouldn’t have to pay any tax up to £300,000, and would have to pay 5% on the portion from £300,001 to £500,000. If the price went above £500,000, usual rates would apply.

What about second homes?

People buying a second home – meaning they own more than one property – have to pay 3% on top of the normal stamp duty rates for a property costing £40,000 or more.

What are the new changes?

Sunak has abolished stamp duty on homes worth up to £500,000, with the change coming into effect immediately and remaining in place until March 31 next year.

This has implications for first-time buyers, who currently have to pay tax on this threshold, as well as existing homeowners looking to move somewhere else.

Those buying second homes will now have to pay 3% stamp duty up to £500,000.

Sunak said the average stamp duty bill will fall by £4,500. Analysis by Savills estate agents found the move would make 88% of English property transactions exempt from the tax, The Telegraph reported, and could actually save the average buyer almost £7,000.

House prices in June 2020 were 2.5% higher than this time last year, according to the latest Halifax House Price Index.